By the time you’re reading this, we’re already well into February (hi from Feb 24 👋), which is actually a perfect time to talk about January.

Because real estate data always lags a bit: January’s numbers reflect what closed and recorded last month, while the day-to-day market we’re living in right now is already starting to shift as spring energy creeps in. We’ll get February’s stats in early March, and that report will give us the clearest look at how this early spring momentum is really playing out.

For now, here’s what January told us — and what it means heading into the rest of Q1.

The numbers that actually matter

Let’s keep this simple and useful. Here’s the Denver Metro snapshot for January:

-

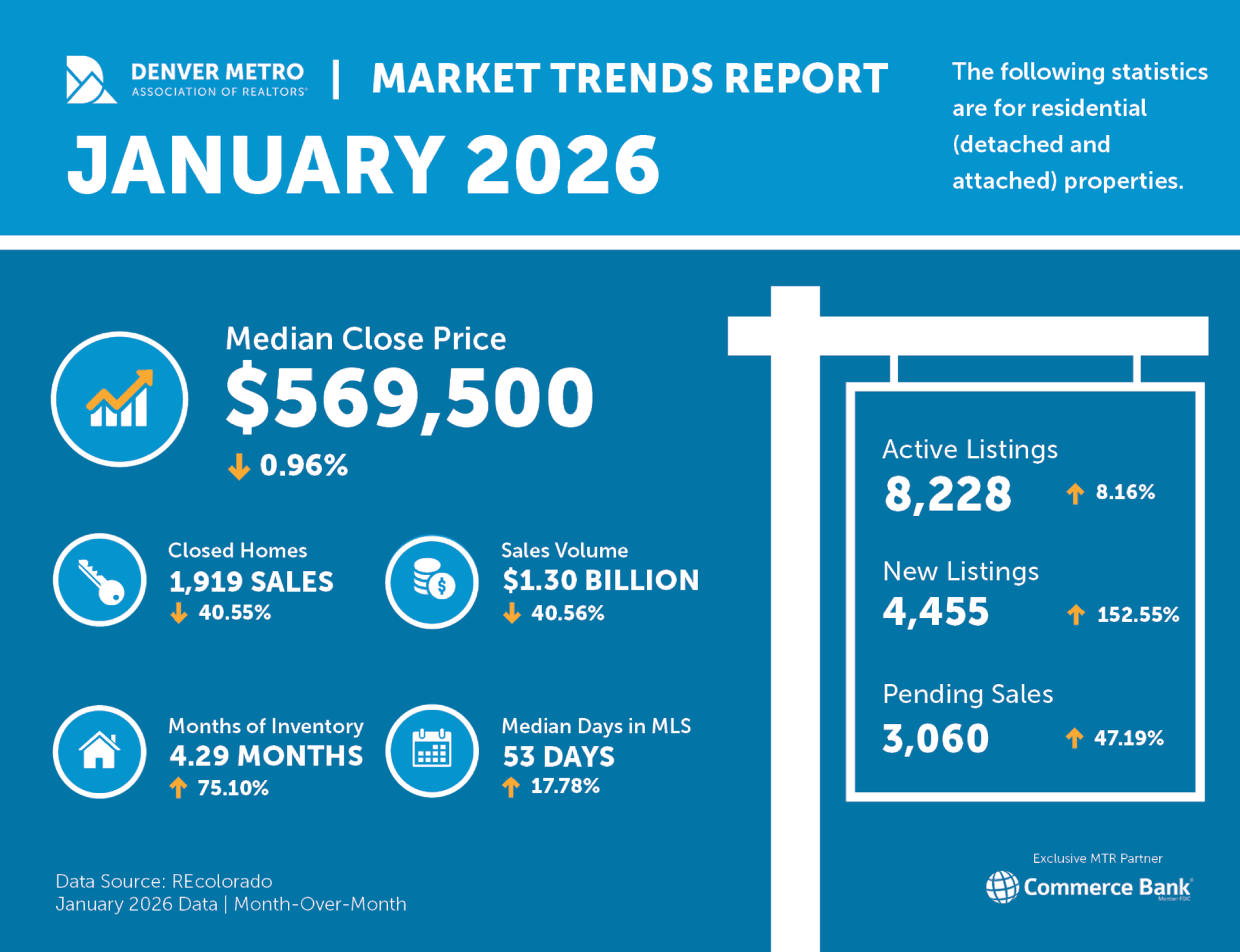

Median close price: $569,500 (down 0.96% month-over-month)

-

Active listings: 8,228 (up 8.16%)

-

New listings: 4,455 (up 152.55% — the “New Year, new listing” effect is real)

-

Pending sales: 3,060 (up 47.19% — buyers are making moves)

-

Closed homes: 1,919 (down 40.55% — January closings are always lighter)

-

Median days on market: 53 days (up 17.78%)

-

Months of inventory: 4.29 months (up 75.10%)

-

Sales volume: $1.30B (down 40.56%)

If you read nothing else, read this: buyers have more options than they’ve had in a while, and homes are taking longer to sell unless they’re positioned perfectly.

What’s really happening out there

The Denver market still feels like it’s carrying the weight of the past few years — higher rates, affordability pressure, and a lot of “waiting to see what happens.”

But January brought a shift that matters:

1) Inventory is building, and buyers can breathe again

With 4.29 months of inventory and a median of 53 days on market, we’re in a market where buyers can slow down, compare options, and negotiate with more confidence. This is not the same environment as the “write today or lose it forever” frenzy.

It’s more thoughtful. More balanced. More normal.

2) Buyers are active — just pickier (and honestly, they should be)

Pending sales jumped 47%, which tells me buyers are absolutely in the game… they’re just being selective.

They’re prioritizing:

-

layout and livability

-

condition

-

location

-

and whether the monthly payment makes sense

Homes that hit that sweet spot are still moving. Homes that don’t? They sit, and then the conversation changes.

3) Pricing sensitivity is real, and it’s the difference-maker

The median close price dipped a touch month-over-month, but what’s more telling is the behavior behind the number: buyers are not overpaying just to “win.”

In this market, the listings that move are the ones that are:

-

priced with today’s reality in mind

-

presented well (photos + staging + prep)

-

and positioned with a clear plan

Pricing isn’t a flex right now. It’s a strategy.

4) It’s still a “two-market” situation

This is the part I want sellers to really hear.

There are basically two experiences happening at once:

Market A:

Well-prepared, well-located, correctly priced homes → still get strong activity (and sometimes competition).

Market B:

Overpriced, underprepared, or hard-to-understand listings → sit longer, require price adjustments, and invite negotiation.

Same city. Same week. Completely different outcomes.

What this means if you’re buying

This is a market of opportunity — not because everything is suddenly “cheap,” but because you have leverage and options.

You can negotiate:

-

inspection items more thoughtfully

-

concessions (depending on the home)

-

terms that protect you (instead of making emotional decisions)

The win right now is being prepared enough to act when the right home shows up — not rushing on the wrong one because you’re afraid it won’t.

What this means if you’re selling

You can absolutely sell well in this market. The path is just different than it was a few years ago.

The sellers who win are the ones who:

-

price realistically

-

invest in first impressions (photos + prep)

-

anticipate inspection conversations

-

and have a real plan from day one

Hope is not a marketing strategy. Preparation is.

My take heading into spring

January brought a meaningful surge in new listings, and buyer activity followed right behind it. And now that we’re nearing the end of February, I’m watching closely to see whether that momentum holds — because February’s report (coming in early March) will tell us if this is a true spring wake-up, or just a post-holiday pop.

Either way, the theme is clear: strategy wins.